Introduction

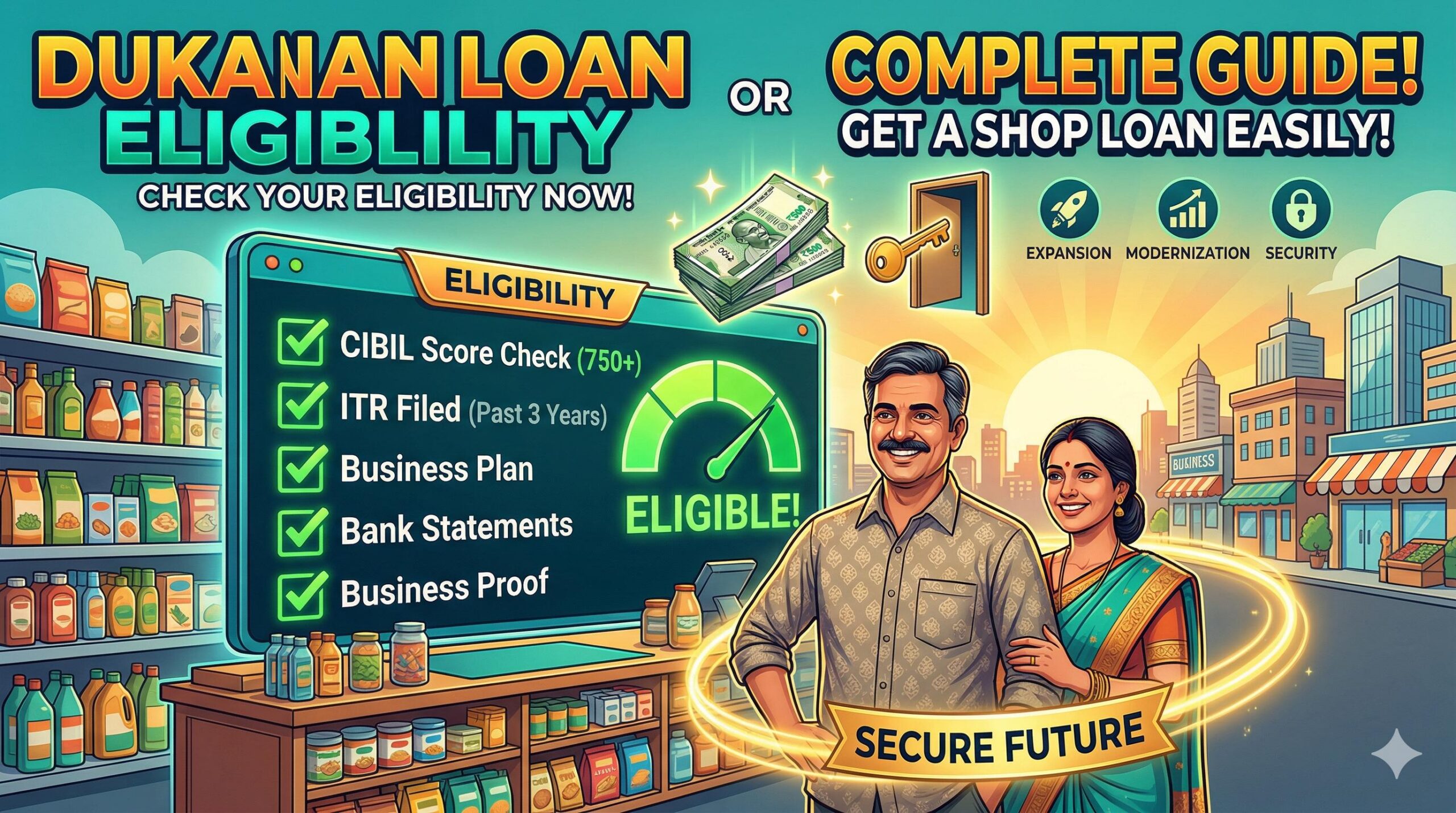

For countless Indian middle-class families and ambitious individuals, opening a local dukan (shop) or expanding an existing retail business is the ultimate path to financial independence. However, transitioning from a business idea to a fully stocked, running store requires capital. While taking a business loan is a standard step, many aspiring shopkeepers face the heartbreak of sudden loan rejections simply because they do not understand dukan ke liye loan eligibility.

Securing funds from a formal bank is not based on luck or having a great business idea; it is strictly based on a set of financial parameters that prove your reliability.

In this comprehensive guide, we will break down exactly what makes you eligible for a shop loan, how a lack of awareness can push you toward dangerous financial traps, and the practical daily habits you must adopt to build a strong, rejection-proof financial profile. Understanding these rules is your first step toward protecting your family’s wealth and safely scaling your business.

Disclaimer: This article is for educational purposes only. It is not professional financial advice. Please consult a certified financial advisor or your bank for specific credit-related decisions.

Table of Contents

The Hidden Risks of Ignoring Loan Eligibility

Many salaried employees and budding entrepreneurs make the mistake of assuming that having a good business idea is enough to get a bank loan. They walk into a bank or apply online without first checking their dukan ke liye loan eligibility. This lack of financial awareness creates massive hidden risks.

The most immediate risk is the damage to your financial identity. Every time you apply for a loan, the bank performs a “hard inquiry” on your CIBIL report. If you do not meet the basic eligibility criteria and get rejected, that rejection stays on your record. If you apply to five different banks in panic, your credit score will drop significantly, making you look “credit-hungry” and desperate.

Once rejected by the formal banking system, the secondary risk kicks in: falling prey to fraud and informal lenders. In India, many small shopkeepers are targeted by scammers offering “guaranteed shop loans without CIBIL” in exchange for a high upfront processing fee. Once the fee is paid, the scammer disappears. Alternatively, shop owners are forced to borrow from local sahukars (informal moneylenders) who trap them in endless cycles of unmanageable debt.

The Financial Impact: How Poor Eligibility Drains Your Wealth

Failing to meet dukan ke liye loan eligibility does not just delay your business plans; it actively drains your hard-earned wealth. Let us look at the financial impact of having to borrow outside the formal banking system because you did not meet the eligibility for a formal loan.

Imagine you need ₹5 Lakhs to expand your grocery store (Kirana shop) or buy new inventory.

- The Formal Route (Eligible): If you meet the eligibility criteria, you could qualify for a government-backed scheme like the PM Mudra Yojana or a standard MSME bank loan. Your interest rate might be around 9% to 12% per year.

- The Informal Route (Ineligible): If you are rejected and go to an informal moneylender, they typically charge interest at a “flat rate” per month—often 2% to 3% monthly. This translates to an astronomical 24% to 36% per year.

Over a 3-year repayment period, borrowing from an informal lender because you failed bank eligibility could cost you lakhs of rupees in extra interest. That is money that should have been your business profit or your family’s savings. Therefore, building your eligibility is quite literally a wealth-saving strategy.

Essential Habits to Build Dukan Ke Liye Loan Eligibility (Prevention)

To protect your finances, avoid loan rejection, and secure the lowest possible interest rates, you must proactively build your eligibility. Adopting these preventive financial habits will make your shop highly attractive to lenders.

1. Maintain a Flawless CIBIL Score

Your personal and business credit scores are the ultimate gatekeepers. A score above 750 tells the bank that you are a safe bet.

The Habit: Never miss an EMI on your personal loans, two-wheeler loans, or credit cards. Pay your bills strictly on time. If you have no credit history, start by getting a secured credit card against a Fixed Deposit (FD) and use it responsibly to build a good score before applying for a shop loan.

2. Register Your Business Legally (Proof of Vintage)

Banks need proof that your shop actually exists and is not a temporary setup. “Business vintage” is a major part of dukan ke liye loan eligibility. Most banks require a minimum vintage of 1 to 3 years.

The Habit: Immediately register your shop. Get a Shop and Establishment Act License (often called a Gumasta license), register for MSME Udyam Aadhaar, and obtain a GST number if your turnover requires it. These legal documents prove to the bank that your business is stable and recognized.

3. Separate Personal and Business Finances

Mixing your household grocery expenses with your shop’s daily earnings in a single savings account is a massive red flag for banks. It makes it impossible for them to assess your true business income.

The Habit: Open a dedicated Current Account for your shop. Ensure that all customer payments (UPI, card machines, cash deposits) go exclusively into this account. A healthy Average Monthly Balance (AMB) in your current account is a strong eligibility booster.

4. File Income Tax Returns (ITR) Consistently

Banks do not give loans based on how much cash is in your cash register; they give loans based on officially documented income.

The Habit: File your Income Tax Returns (ITR) every year, even if your income is below the taxable limit. For shop loans, banks will almost always ask for the last 2 to 3 years of ITR and your Profit & Loss (P&L) statements. Consistent ITR filing proves your business is generating sustainable income.

Smart Money Behavior Beyond the Loan

Understanding your dukan ke liye loan eligibility is just the first step. True financial awareness involves managing the borrowed money smartly so that your business thrives and your family remains secure.

First, practice strict budgeting. Before applying for a loan, calculate the exact amount you need for your shop—do not borrow ₹10 Lakhs just because you are eligible if your actual requirement is only ₹4 Lakhs. Extra loan money means extra interest, which eats into your daily profits. Use an online EMI calculator to ensure that the monthly installment will not choke your shop’s cash flow during slow business months.

Second, build a business emergency fund. Do not rely entirely on the daily cash flow of the shop to pay the loan EMI. Smart money behavior means saving at least three to six months’ worth of EMI payments in a separate liquid mutual fund or fixed deposit. If your shop faces an unexpected closure or a sudden drop in sales, this emergency fund will ensure your EMI is paid on time, protecting your CIBIL score and your future eligibility.

Lastly, stay vigilant against financial fraud. Remember that no legitimate bank or NBFC will ever ask you to pay a “file charge” or “processing fee” directly to a personal UPI ID or bank account before approving your loan. Processing fees are always deducted directly from the final loan amount. By combining strict eligibility preparation with high financial literacy, you will ensure that your shop grows safely, bringing long-term prosperity to your family.

Proven CIBIL Score Badhane Ke Tips: Secure Your Financial Future Today

Frequently Asked Questions (FAQs)

1. Can I get a dukan loan without a CIBIL score? If you have never taken a loan or a credit card before, your CIBIL score will be “NA” or “NH” (Not Applicable/No History). While some banks offer small starter loans or government schemes like the Shishu category of PM Mudra Yojana to new borrowers, it is generally much harder. It is highly recommended to build a credit history first using a secured credit card before applying for a large business loan.

2. Is a GST number compulsory for shop loan eligibility? Not always. For very small shops with a turnover below the government’s mandatory GST registration threshold (usually ₹40 Lakhs for goods), a GST number is not legally required. However, you must provide other valid business proofs, such as a Shop and Establishment License (Gumasta) or an MSME Udyam Registration certificate, to prove your shop is legitimate.

3. What is the PM Mudra Yojana, and is it good for small shops? The Pradhan Mantri Mudra Yojana (PMMY) is a highly beneficial government scheme designed specifically to provide loans up to ₹10 Lakhs to non-corporate, non-farm small businesses and shops. It is an excellent option for Indian middle-class shopkeepers because it offers formal credit at reasonable interest rates without requiring collateral (property security).

4. Can I get a business loan if my shop is run from a rented property? Yes, absolutely. Most retail shops in India operate from rented spaces. To prove your business vintage and stability, you simply need to provide a valid, legally registered Rent Agreement along with utility bills (like an electricity bill) in the landlord’s name, accompanied by a No Objection Certificate (NOC) if required by the bank.

5. Beware of Scams: Do I have to pay an advance fee to get my shop loan approved? No! This is the most common financial fraud targeting small business owners. Legitimate banks and regulated NBFCs will never ask you to transfer an “advance processing fee” or “file charge” via UPI or into a personal bank account before approving the loan. Official processing fees are always deducted directly from the final loan amount disbursed to your account.

Conclusion

Building the right dukan ke liye loan eligibility does not happen overnight, but it is one of the most rewarding financial investments you can make for your business. By consistently practicing smart money habits—such as maintaining a spotless CIBIL score, keeping your personal and business bank accounts separate, and filing your ITR regularly—you transform your shop from a risky venture into a highly trusted business in the eyes of any bank.

Remember, the goal is not just to get a loan; the goal is to access affordable, formal credit that helps your business grow without trapping you in high-interest debt. Stay away from unverified agents promising guaranteed loans, rely on your solid financial documentation, and borrow only what you can comfortably repay. With discipline and financial awareness, you can safely fund your shop’s expansion and secure a prosperous future for your family.