Introduction

In 2026, the financial pressure on Indian middle-class families is heavier than ever before. We are living in a time where the cost of living—from petrol prices to school admissions—is rising much faster than the average salary. For many salaried employees and small business owners, the month often ends with a “zero balance” notification, leading to immense stress and anxiety.

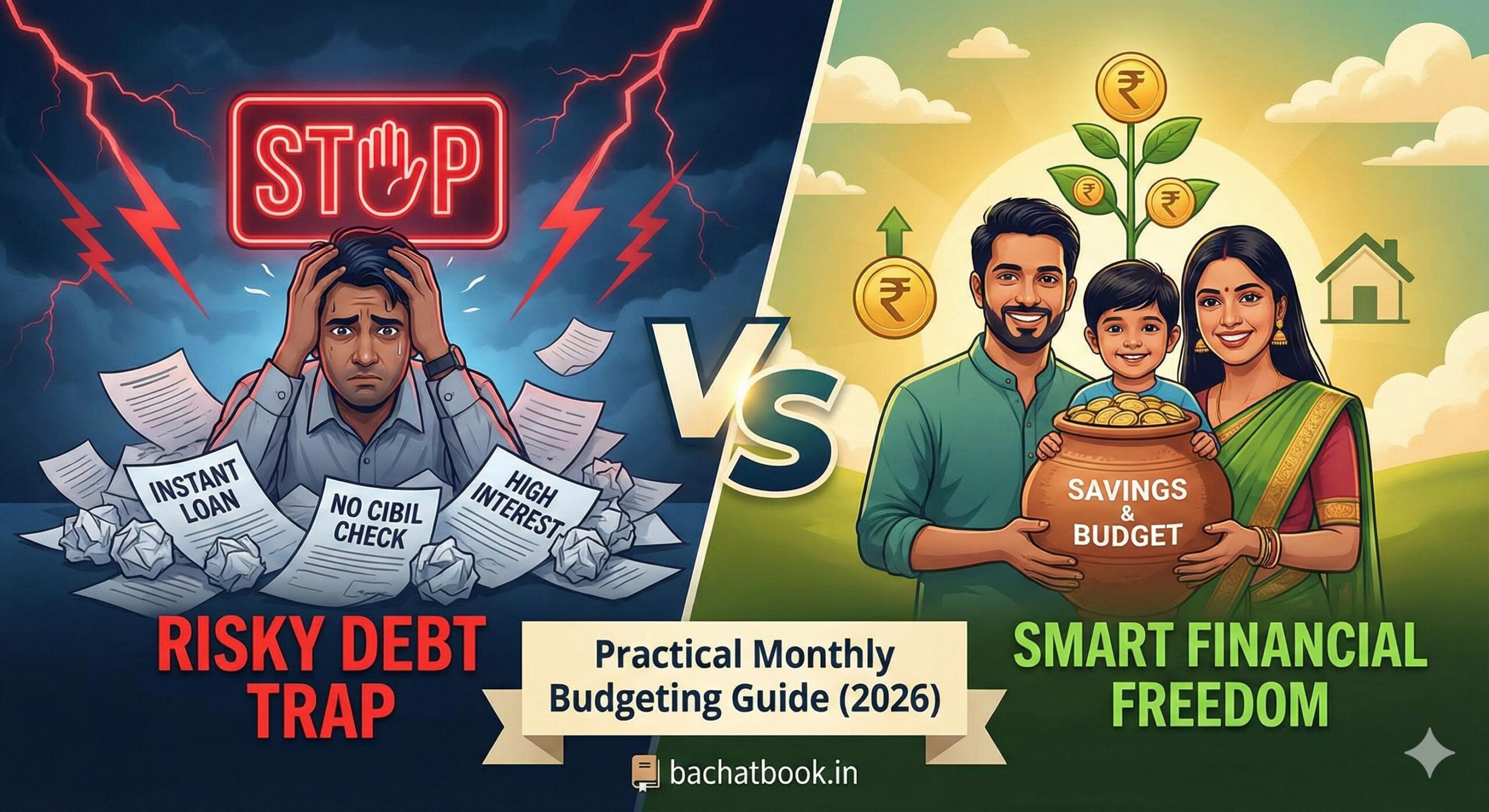

When financial emergencies strike, panic sets in. This is the moment when many people turn to search engines looking for an Instant business loan No CIBIL or high-interest personal loans just to survive the week. While these options might offer temporary relief, they often trap hard-working Indians in a vicious cycle of debt, interest repayments, and financial instability.

But there is a better way. The path to financial freedom does not begin with a loan application; it begins with a notebook, a pen, and a change in mindset. Saving money in India is not just about cutting costs; it is about optimizing how you use your hard-earned money. Whether you are a homemaker managing the kitchen expenses, a student saving pocket money, or a father planning for your child’s future, this guide covers realistic, proven strategies to build a financial safety net. By following these steps, you can stop relying on debt and start building real wealth.

Disclaimer: This article is for educational and informational purposes only. It does not constitute professional financial advice. We do not provide loans, investment services, or guarantee financial results. Please consult a certified financial advisor before making major financial decisions.

Table of Contents

Why Saving Money Is Important in India

In Indian culture, saving money has always been considered a virtue. Our grandparents believed in saving for a rainy day, often keeping cash hidden in rice tins or locking it in bank Fixed Deposits (FDs). However, in today’s digital spending era, this habit is fading. Here is why reviving the habit of saving is critical for your survival and growth.

The Emergency Fund Barrier

Life is unpredictable. A sudden medical emergency requiring hospitalization in a private facility can cost lakhs of rupees. A sudden breakdown of your car or a necessary home repair can derail your monthly budget instantly. Without a solid “Emergency Fund”—usually 3 to 6 months of expenses kept in a savings account—you are vulnerable. This vulnerability is what forces people to look for desperate measures like an Instant business loan No CIBIL, which often come with predatory interest rates. Having your own savings means you are your own bank during tough times.

Family Responsibilities & Social Obligations

In India, our financial responsibilities extend beyond ourselves. We often support aging parents, contribute to the extended family, and participate in social functions. Weddings, festivals like Diwali, and family gatherings require significant spending. If you do not save specifically for these “expected” expenses, they will feel like “unexpected” burdens when the time comes.

Job Market Uncertainty

The corporate sector and even traditional businesses are facing rapid changes due to technology and automation. Layoffs, salary delays, or reduced bonuses are becoming common realities. Relying 100% on your next paycheck is a high-risk strategy. Savings provide you with a “runway”—a period of time you can survive without a job while you look for a better opportunity, ensuring you don’t make desperate career choices out of fear.

Future Goals and Inflation

Education inflation in India is typically higher than general inflation. The cost of an engineering or medical degree today will likely double in the next 7-10 years. Similarly, buying a home in a tier-1 or tier-2 city requires a massive down payment. Small, consistent savings today are the only way to build the corpus needed for these major life milestones without drowning in EMI debt.

Common Reasons Indians Fail to Save Money

Many people have the intention to save, but they fail to execute it. Understanding the psychological and practical barriers is the first step to overcoming them.

Lack of Budgeting and Tracking

The biggest enemy of saving is “mental accounting.” Many people believe they know where their money goes, but they are often wrong. Without writing down expenses, small leaks sink the ship. That ₹50 coffee, the ₹200 subscription, and the ₹100 delivery fee add up to thousands by month-end. If you do not tell your money where to go, you will wonder where it went.

Impulse Spending & The “Sale” Trap

E-commerce giants and quick-commerce apps have made spending money too easy. The “Fear Of Missing Out” (FOMO) during the Great Indian Festival or Big Billion Days drives people to buy things they do not need simply because they are on a 50% discount. Remember, if you buy a ₹20,000 item for ₹10,000 just because it was on sale, you didn’t save ₹10,000; you spent ₹10,000.

The EMI Trap

“No Cost EMI” is a marketing term that has ruined many budgets. It makes expensive items look affordable by breaking the price down into small monthly chunks. A ₹80,000 phone seems cheap at ₹4,000 a month. However, when you stack 4 or 5 such EMIs (phone, TV, fridge, laptop), a huge portion of your future income is already spent before you even earn it. This reduces your liquidity and prevents you from saving.

Lifestyle Inflation

This is a common phenomenon among young earners. As soon as you get a promotion or a salary hike, your expenses immediately rise to match the new income. You upgrade from a bike to a car, from a rented apartment to a bigger one, or from local brands to luxury brands. Because your spending grows with your income, your savings rate remains zero.

Step-by-Step Monthly Budgeting Method

The most effective way to save is to follow a logical structure. We recommend the 50-30-20 Rule, customized for the Indian context. Let’s break this down assuming a net take-home salary of ₹50,000.

Step 1: Calculate Net Income

This is the amount that actually hits your bank account after Provident Fund (PF), Tax (TDS), and other deductions. Do not budget based on your “CTC” (Cost to Company); budget based on your “Cash in Hand.”

Step 2: Fixed Expenses (Needs) – 50% (₹25,000)

These are survival expenses. You cannot avoid them.

- Housing: Rent or Home Loan EMI.

- Utilities: Electricity, Water, Gas cylinders, Mobile bills, Broadband.

- Groceries: Ration, milk, vegetables, fruits.

- Education: School fees, tuition fees, books.

- Transport: Metro card recharge, petrol/diesel, bus fare.

Guidance: If your needs exceed 50% of your income, you are in the “danger zone.” You may need to look for cheaper accommodation or reduce utility usage immediately.

Step 3: Variable Expenses (Wants) – 30% (₹15,000)

These are lifestyle choices. These make life enjoyable but are not essential for survival.

- Entertainment: Movies, OTT subscriptions (Netflix/Hotstar/Prime).

- Dining Out: Weekend dinners, ordering via Zomato/Swiggy.

- Shopping: Clothes, accessories, gadgets.

- Hobbies: Gym memberships, travel.

Guidance: This is the first place to cut when you are short on cash. If you are searching for an Instant business loan No CIBIL to fund a vacation or a new phone, you are making a critical financial mistake. Stop spending here immediately.

Step 4: Savings & Investments – 20% (₹10,000)

This category is for your future self. It should be treated as a “bill” you must pay to yourself.

- Emergency Fund: Keep cash in a liquid fund or savings account.

- Investments: SIPs in Mutual Funds, PPF (Public Provident Fund), or Recurring Deposits (RD).

- Insurance: Term Life Insurance and Health Insurance premiums (essential protection).

Guidance: Automate this. Set a standing instruction so that as soon as your salary is credited, 20% is automatically moved to a separate investment or savings account.

Smart Money Saving Tips for Indian Households

Every Indian household has “hidden money” lying in wastage. Here is how to find it.

Grocery Savings Secrets

- The List Rule: Never go to the supermarket or open a grocery app without a prepared list. Stick to the list strictly.

- Buy Seasonal: In India, vegetables and fruits have seasons. Buying cauliflower (Gobi) in summer or mangoes in winter will cost you double. diverse your diet based on what is abundant and cheap in the market.

- Wholesale vs. Retail: For non-perishable items like Rice (Chawal), Wheat Flour (Atta), Pulses (Dal), and Oil, buy in bulk (5kg or 10kg packs) from wholesale markets (Mandis) or D-Mart style stores. The per-unit cost is significantly lower than buying 1kg packs weekly.

Electricity & Gas Optimization

- Phantom Power: Switch off the main plug for TVs, Microwaves, and Computers when not in use. Even in standby mode (red light on), they consume electricity.

- AC Economy: Running an AC at 24 degrees is healthy and consumes much less power than running it at 18 degrees. Use a fan along with the AC for better circulation.

- Cooking Gas: Ensure your gas burner flame is blue. A yellow flame indicates wastage. Always soak dals and rice before cooking; this reduces cooking time and saves gas.

Transport Hacks

- Carpooling: If you drive to work, use apps to offer rides or share a ride with colleagues. It splits the fuel cost.

- Two-Wheeler Maintenance: Keep your bike’s tires inflated to the correct pressure. Low air pressure increases fuel consumption.

- Public Transport: In cities like Delhi, Mumbai, or Bangalore, the Metro or local train is not only cheaper but often faster than taking a cab during peak traffic.

Saving Money for Students & Young Earners

for future savings")

If you are a student or in your first job, you have the greatest asset of all: Time. Compound interest works best when you start early.

Pocket Money Management

Treat your pocket money like a salary. If you receive ₹2,000 a month, try to save ₹500. Open a zero-balance savings account and deposit this amount. Do not touch it. By the end of the year, you will have ₹6,000 plus interest—enough for a course or a small trip.

The “Latte Factor” (Chai/Sutta Cost)

Small daily habits drain wallets. A ₹20 chai and a ₹15 snack twice a day equals ₹70 daily. That is ₹2,100 a month and roughly ₹25,000 a year! We aren’t saying don’t enjoy chai, but be aware of how much “small” spending costs you annually.

Used Books and Resources

Never buy brand new textbooks unless necessary. Look for seniors selling old books, visit second-hand book markets (like Daryaganj in Delhi or College Street in Kolkata), or use digital PDFs.

Avoid Debt Traps

Banks love to offer “Lifetime Free Credit Cards” to young earners. Be very careful. If you miss one payment, the interest rate can be 40% per annum. Using credit responsibly is good, but using it to buy things you can’t afford is the path to ruin.

Bachat Gat Loan Process 2026: Complete Guide & Smart Saving Tips for Indian Families

Digital Tools That Help Save Money

Use your smartphone to save money, not just to spend it.

- Expense Tracking Apps: Use apps (like Walnut, Moneyfy, or Splitwise) that read your transaction SMS and automatically categorize your spending into “Food,” “Travel,” and “Shopping.” This gives you a clear pie chart of your expenses at the end of the month.

- Price History Trackers: Before buying anything on Amazon or Flipkart, use a price tracker extension to see if the “discount” is real or fake.

- UPI Limits: Many UPI apps allow you to set a daily transaction limit. Set a limit for yourself (e.g., ₹500 per day for casual spending). If you cross it, the app will block the transaction, forcing you to rethink the purchase.

Long-Term Saving Habits Indians Should Build

The 24-Hour Rule

Whenever you feel the urge to buy something expensive (over ₹2,000), wait for 24 hours. Do not buy it immediately. In 80% of cases, the urge to buy will fade away by the next morning, proving it was an impulse want, not a need.

Goal-Based Saving

Don’t just save for “saving’s sake.” Give your money a name.

- Open a Recurring Deposit (RD) named “Diwali Gift Fund.”

- Open a Liquid Fund named “Emergency Medical Fund.”

- Open a Mutual Fund named “New Car Fund.” When you see the name, you are less likely to withdraw that money for a trivial reason like buying a pizza.

Periodic Review (The Sunday Ritual)

Every Sunday night, spend 15 minutes reviewing your bank statement or UPI history. Identify one expense from the last week that was unnecessary and promise to avoid it next week.

Frequently Asked Questions (FAQ)

How much of my salary should I realistically save in India? The golden rule is 20%. However, if you are living in a metro city with high rent and a low starting salary, this might be hard. Start with 5% or 10%. The habit of saving is more important than the amount initially. As your income grows, increase the percentage.

Is budgeting necessary if I have a low income? Yes, budgeting is actually more critical for low-income households. When resources are limited, every rupee must be assigned a specific job to ensure rent and food are covered. Budgeting prevents you from falling into the trap of high-interest loans.

I have no CIBIL score. Is an “Instant business loan No CIBIL” a good option for emergencies? We strongly advise against this. Lenders who offer loans without checking CIBIL scores often charge exorbitant interest rates (sometimes 1% per day) and use aggressive recovery tactics. It is better to liquidate gold, borrow from family, or use your emergency fund. Avoid these loans to keep your financial health safe.

How can I save money on Indian weddings? Indian weddings are major expense events. To save: limit the guest list to close family and friends, rent wedding jewelry and clothes instead of buying, choose an off-season date for the venue, and minimize the number of food items on the menu (focus on quality over quantity).

What is the best way to start investing for a beginner? Start with a Recurring Deposit (RD) in your bank for guaranteed safety. Once you have some savings, start a SIP (Systematic Investment Plan) in an Index Mutual Fund (like Nifty 50) for long-term growth. Always consult a financial advisor.

How do I stop overspending on online food delivery? Delete the apps from your phone during weekdays. Meal prep on Sundays so you have food ready in the fridge. Calculate the annual cost of your orders—seeing that you spent ₹40,000 on delivery last year is usually enough motivation to stop!

Conclusion

Saving money is not about living a miserable, restricted life. It is about taking control. It is about prioritizing your peace of mind over temporary pleasures. When you have money in the bank, you walk with confidence. You don’t fear the end of the month, and you certainly don’t need to panic search for an Instant business loan No CIBIL when a small crisis hits.

Budgeting is a skill, like driving or cooking. You might make mistakes in the first month, but don’t give up. Stick to the 50-30-20 rule, track your small expenses, and cut down on wasteful habits. Remember, every big ocean is made of little drops of water. Start your savings journey today, and your future self will thank you.