Introduction: Rebuilding Trust with the Banking System

Getting a personal loan or a standard credit card rejected when you desperately need funds is a highly stressful experience for any middle-class family. Usually, this rejection points to a damaged credit history caused by past financial mistakes. While the internet is flooded with fake agents promising overnight magic, the safest, most reliable, and completely legal method to rebuild your financial reputation is a secured credit card CIBIL fix.

This method allows you to leverage your own savings to prove your creditworthiness to the banking system. By opening a Fixed Deposit (FD) and getting a card issued against it, you bypass the traditional credit check entirely. However, stepping back into the credit system requires extreme caution and financial awareness. This guide will walk you through exactly how secured cards work, the hidden debt traps that can wipe out your hard-earned savings, and the smart money habits necessary to protect your data while successfully repairing your score.

Table of Contents

The Hidden Risks of Credit Repair

When salaried employees or students face loan rejections due to a low credit score, panic often sets in. This desperation makes them vulnerable to significant digital and financial risks, which can be avoided by understanding how a secured card works.

The “CIBIL Repair Agency” Scam

The biggest risk when trying to fix your credit is falling for fraudulent “credit repair agencies.” These scammers advertise on social media or send WhatsApp messages promising to legally remove negative remarks or defaults from your CIBIL report for a fee of ₹5,000 to ₹10,000. This is a complete scam. No third-party agency can magically erase factual banking history. The only genuine way to improve your score is through a secured credit card CIBIL fix and time. Sharing your PAN card and Aadhaar details with these fake agencies often leads to identity theft and unauthorized loans taken in your name.

The Risk of Card Mismanagement

A secured credit card looks, feels, and swipes exactly like a normal unsecured credit card. The risk here is psychological. Because it functions so smoothly, many borrowers forget that the card is tied to their life savings (the FD). If you treat this card as “free money” rather than a strict credit-building tool, you risk losing the very savings you pledged to the bank.

Data Theft and Phishing

Just because your card is secured by an FD does not mean it is safe from cybercriminals. Scammers frequently target people with new credit cards by calling them, pretending to be bank executives offering “limit upgrades” or “KYC updates,” aiming to steal the card’s CVV and OTP.

Financial Impact: The Cost of Misusing Your Secured Card

Using a secured credit card to fix your CIBIL score is a brilliant strategy, but if mismanaged, the financial consequences are severe and directly impact your household budget.

Complete Loss of Your Fixed Deposit

Usually, banks offer a credit limit that is 80% to 90% of your FD amount. For example, an FD of ₹20,000 might give you a limit of ₹18,000. If you exhaust this limit and fail to pay the credit card bill for a consecutive period (usually 60 to 90 days), the bank has the legal right to liquidate (break) your Fixed Deposit. They will use your FD money to clear the outstanding credit card dues, wiping out your savings instantly.

The “Minimum Amount Due” Debt Trap

Credit cards carry the highest interest rates in the financial market, often ranging from 36% to 42% Annually (APR). If you receive your monthly statement and choose to pay only the “Minimum Amount Due” (which is usually just 5% of the total bill), the remaining balance immediately starts attracting this massive interest. The interest compounds daily, turning a small shopping bill into a massive financial burden that eats into your monthly salary.

Double Damage to Your Credit Score

The entire purpose of a secured credit card CIBIL fix is to build a positive payment history. If you default on a secured card, the bank will report this fresh default to CIBIL and Experian. A default on a secured product is viewed very harshly by the financial system. It will plunge your score even lower than before, keeping you locked out of the formal banking system for years.

Prevention Habits: How to Protect Your Money and Score

To safely execute a secured credit card CIBIL fix without putting your finances at risk, you must adopt strict, non-negotiable preventive banking habits.

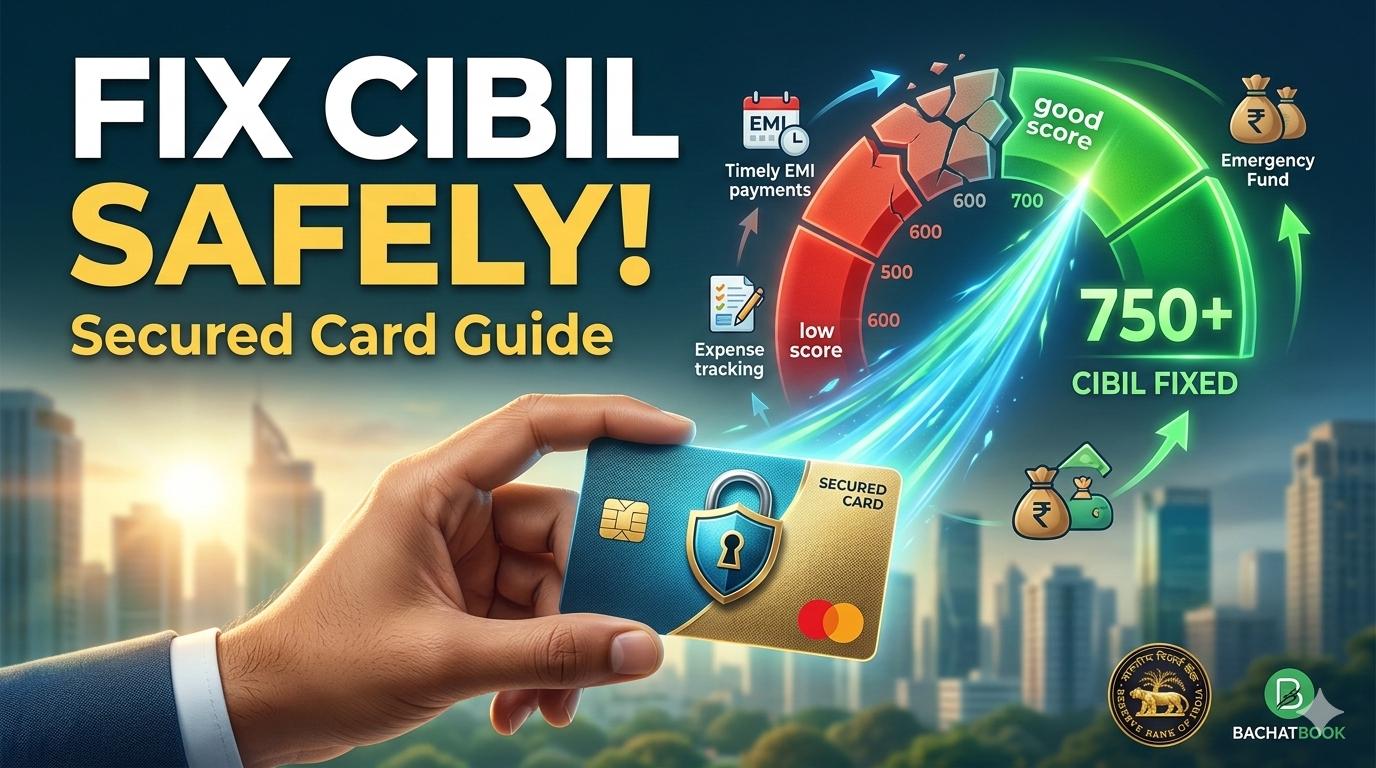

- The 30% Utilization Rule: Never spend the entire limit of your secured card. If your limit is ₹18,000, try to never spend more than ₹5,400 (30%) in a single billing cycle. High credit utilization signals to credit bureaus that you are “credit hungry,” which can actually drop your score instead of fixing it.

- Always Pay the Total Outstanding Balance: Make it a strict habit to pay 100% of the “Total Amount Due” three days before the due date. Never use the “Minimum Amount Due” option. Paying in full ensures you never pay a single rupee in interest, making the card completely free to use.

- Setup Auto-Debit from a Salary Account: Do not rely on your memory to pay the bill. Link your secured credit card to your primary salary or bachat (savings) account using an auto-debit mandate. This ensures the bill is paid automatically, eliminating the risk of late fees and negative CIBIL reporting.

- Keep the FD untouched for 12-18 Months: Rebuilding trust takes time. Do not break the FD or close the secured card after just three months. Keep the account active, use it for small bills (like mobile recharges or electricity bills), and pay it off immediately. You need at least 12 to 18 months of consistent history to see a major jump in your CIBIL score.

Smart Money Behavior: Building a Sustainable Future

A secured credit card is a medical treatment for a sick credit profile; it is not extra income. True financial stability comes from fundamentally changing how you view money and debt.

Treat Credit as Cash

Smart money behavior means never swiping your secured card for an amount that you do not already have sitting in your bank account. If you want to buy a ₹5,000 appliance, check your debit account first. If the money is there, swipe the credit card to get the CIBIL benefit, and immediately transfer the money from your bank to pay the card bill.

Focus on Bachat (Savings) First

While you are using the secured card to fix past mistakes, you must also protect your future. Do not rely on credit cards for emergencies. Actively build an emergency cash fund. Saving even ₹1,000 to ₹2,000 every month in a separate account ensures that if a medical emergency or urgent repair arises, you use your own money instead of taking on high-interest debt.

Graduate to an Unsecured Card

The ultimate goal of this journey is financial freedom. After 12 to 18 months of perfect payment history, your CIBIL score should cross the 750 mark. At this point, you can apply for a standard, unsecured credit card. Once approved, you can safely close the secured card and get your original Fixed Deposit (along with the earned interest) safely back into your bank account.

Rebuilding your financial reputation is entirely in your hands. By using a secured card responsibly, avoiding quick-fix scams, and respecting your credit limit, you can safely restore your CIBIL score and secure a stronger financial future for your family.

P2P Lending for Low CIBIL: A Safe Borrowing Guide

Frequently Asked Questions (FAQ)

What is the minimum FD amount required for a secured credit card?

In India, most major banks and RBI-registered financial institutions allow you to open a secured credit card with a minimum Fixed Deposit ranging from ₹2,000 to ₹10,000. The credit limit you receive will typically be 80% to 90% of this deposited amount.

How long does a secured credit card CIBIL fix take to show results?

Credit building requires patience. While the bank reports your payment behavior every month, it generally takes 3 to 6 months of consistent, full, and on-time payments to see a noticeable improvement in your CIBIL score. For a complete recovery to a “good” score (750+), you should plan to use the card responsibly for 12 to 18 months.

Will I lose my Fixed Deposit if I close the secured credit card?

No, your money is safe. If you decide to close the secured credit card, you must first clear all outstanding dues on the card. Once the credit card account is officially closed with a zero balance, the bank will release your Fixed Deposit, and the original amount plus the earned interest will be credited back to your savings account.

Can a secured card erase defaults or settled accounts from my CIBIL report?

No financial product or agency can magically erase factual past defaults, late payments, or “settled” remarks from your credit history. A secured card works by adding a thick layer of positive payment history on top of your old mistakes. Over time, this new positive behavior dilutes the impact of the negative remarks, causing your overall score to rise.

Are “CIBIL repair agencies” a safe alternative to a secured card?

Absolutely not. Third-party agencies that ask for upfront fees to “fix” your credit score are almost always scams. They cannot legally alter your credit bureau data. Sharing your PAN, Aadhaar, and banking details with these unregistered agents puts you at a severe risk of identity theft and financial fraud. The DIY secured card route is the only safe and official method.

Conclusion: A Disciplined Path to Financial Recovery

Executing a secured credit card CIBIL fix is not about getting extra money to spend; it is a highly disciplined financial recovery program. By backing your card with a Fixed Deposit, you are taking a safe, RBI-regulated route to rebuild trust with major credit bureaus. The key to your success lies in protecting that FD at all costs.

True financial freedom is built on consistent bachat (savings) and smart digital habits. By strictly utilizing less than 30% of your credit limit, entirely avoiding the “minimum amount due” debt trap, and keeping your banking data safe from phishing scams, you can steadily climb back to a 750+ score. Treat this secured card as a temporary stepping stone. Once your score recovers, graduate to an unsecured card, reclaim your FD, and continue living a debt-free, financially secure life.

Disclaimer: Educational purposes only. This article is designed to provide general information regarding credit scores and financial awareness. It is not professional financial advice. Always read the terms and conditions of any bank or financial institution before opening a Fixed Deposit or applying for a credit card.